Hidden exclusions inside insurance policies determine when coverage applies and when it does not. Many policyholders assume a policy will cover any related loss, but exclusions limit that promise in specific circumstances. Understanding what is excluded helps prevent claiming denials and costly surprises. This article outlines common exclusions, ways to evaluate risks, and practical steps to close important gaps.

Identify Common Policy Exclusions

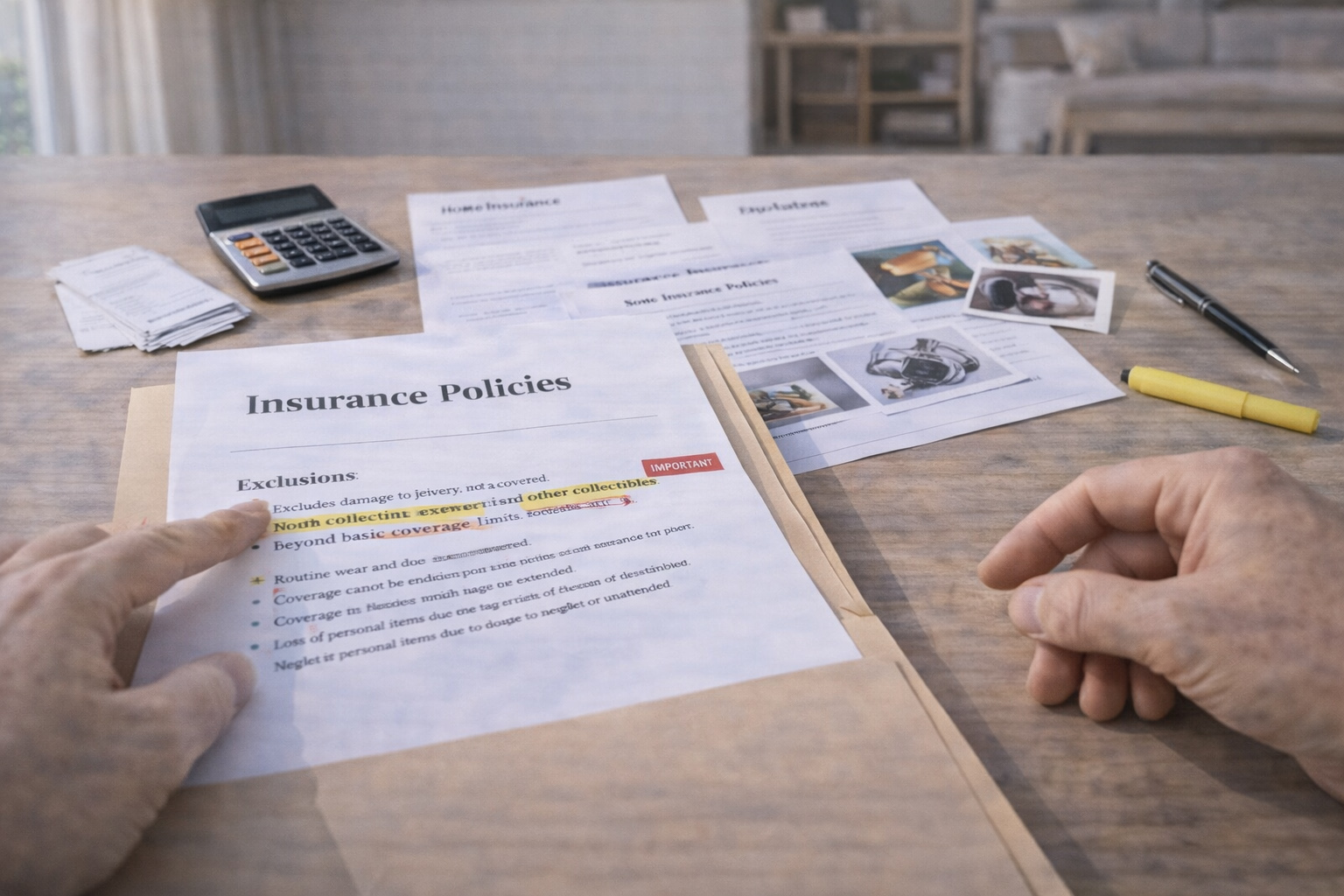

Most standard policies contain several familiar exclusions such as wear and tear, intentional acts, certain natural hazards, and named perils that are not covered unless added. Business-related losses and cyber incidents are frequently excluded from personal policies unless a rider or separate policy is purchased. Some exclusions are conditional, triggering only when specific circumstances apply, which can make interpretation tricky. Reviewing the exclusion language carefully is essential to know where coverage stops.

When you spot exclusions, note whether they are absolute or subject to endorsements. This distinction determines whether you can negotiate or purchase additional coverage to fill the gap.

Assessing Personal Risk and Coverage Gaps

Begin by matching your lifestyle, property, and activities to the policy declarations and exclusions to identify likely gaps. Consider hobbies, home-based businesses, valuable collections, and frequent travel as factors that may create uncovered exposures. Use claim examples and scenario testing to see how exclusions would apply in realistic situations. Consulting an agent or independent advisor can clarify ambiguous language and the typical outcomes of similar claims.

Keep documentation of high‑value items and unusual exposures so you can discuss precise needs with your insurer. That preparation makes it easier to obtain endorsements or separate policies if required.

Practical Steps to Reduce Exposure

There are straightforward actions to address exclusions without sacrificing essential protection. Carefully read your policy declarations and the exclusion section, ask targeted questions, and request written explanations for any unclear clauses. If an exclusion leaves a material gap, seek endorsements, riders, or a specialized policy tailored to that hazard. Maintain reasonable preventive measures and documented maintenance records, since some coverages depend on demonstrated loss prevention.

- Compare endorsements and premium impact before committing.

- Consider umbrella or specialized coverage for high-risk exposures.

- Document communications with your insurer for future reference.

Taking these steps proactively reduces the chance of denial and ensures you have options when common exclusions would otherwise leave you exposed. Periodic reviews align coverage with life changes and evolving risks.

Conclusion

Policy exclusions shape the limits of protection and deserve careful attention. Regularly review your policies and discuss gaps with a qualified advisor. Proactive adjustments and clear documentation help maintain appropriate coverage.