Evaluating insurance can feel overwhelming if you approach it without structure. Start by clarifying what you already have and what gaps might exist. Use simple benchmarks to measure adequacy rather than comparing features in isolation. A clear framework helps you make consistent, confident choices as circumstances change.

Assess Your Current Coverage

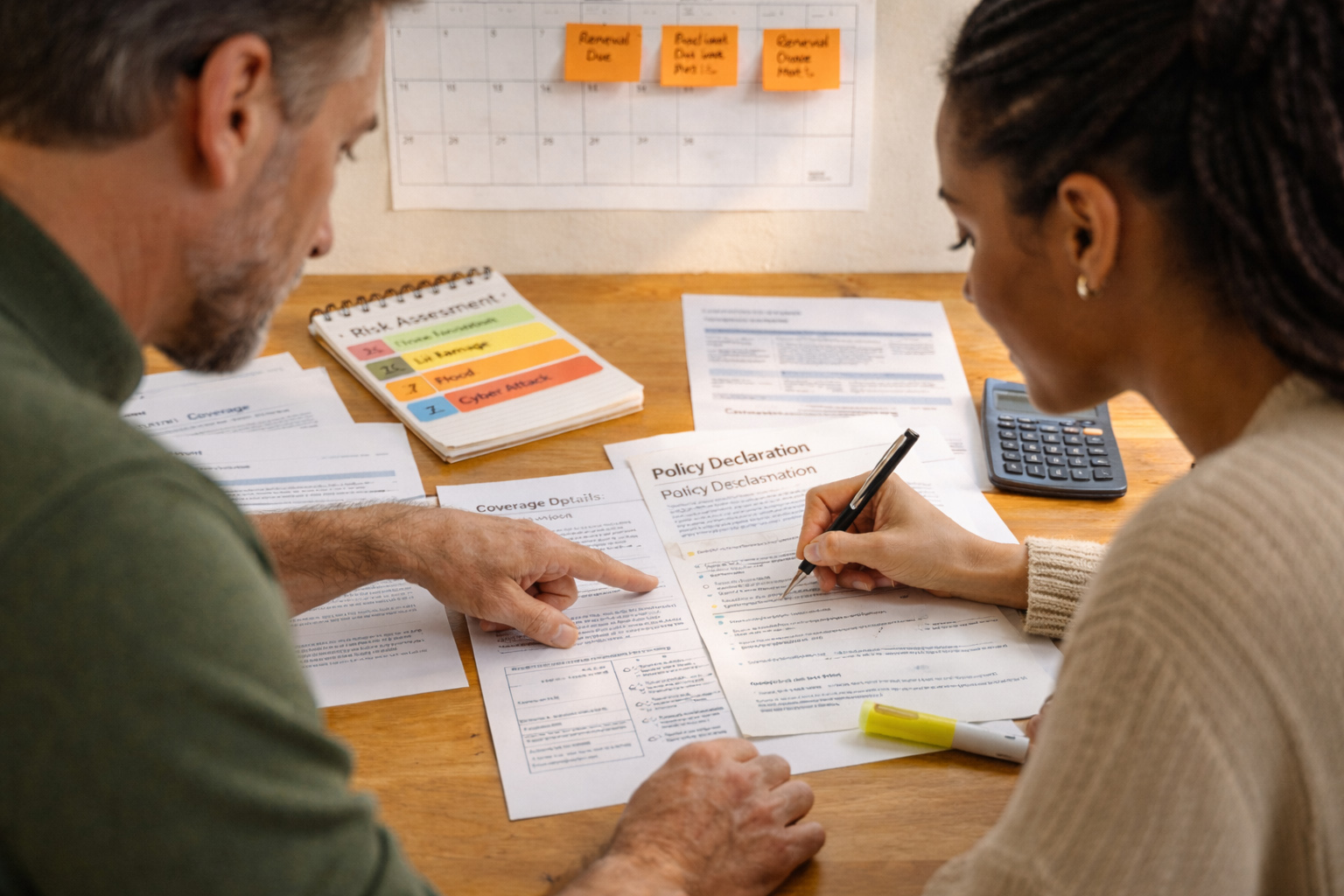

Begin with an inventory of existing policies, limits, and deductibles, and note renewal dates and premium amounts. Review declarations pages and summarize what is covered and what is excluded so you can see patterns. Identify overlap between policies and any protection that is missing or inadequate. This baseline makes it easier to decide what to prioritize when shopping or adjusting coverage.

Focus on clarity rather than perfection when cataloging your coverage. Even a simple spreadsheet or file with key numbers will improve decision making.

Prioritize Risks and Needs

List potential risks and rank them by likelihood and financial impact to your household or business. Consider both short-term disruptions and long-term consequences, such as loss of income or major repairs. Determine which risks would be ruinous without insurance and which you can reasonably self-insure through savings. Align coverage priorities to your risk tolerance and financial capacity.

When priorities are explicit, it becomes easier to decline unnecessary add-ons and keep premiums focused on meaningful protection.

Compare Policies and Costs

Comparing options requires more than price shopping; evaluate policy language, limits, exclusions, and service reputation. Pay attention to definitions and conditions that trigger coverage, as small differences can change outcomes significantly. Use consistent scenarios to test policy responses, and quantify expected out-of-pocket costs under those scenarios.

- Compare premiums, deductibles, and coverage limits together, not separately.

- Check for exclusions that apply to your major concerns.

- Evaluate insurer reputation for claims handling, if available.

Document your comparisons so you can justify choices and revisit them later without starting from scratch.

Maintain and Review Regularly

Insurance needs evolve with life events, asset changes, and shifts in risk exposure, so schedule periodic reviews. Update coverages after major purchases, moves, family changes, or business developments to prevent gaps. Keep records of communications and policy changes to simplify future reviews and claims processes.

Regular reviews also reveal opportunities to bundle or adjust deductibles to improve cost-effectiveness without sacrificing core protection.

Conclusion

Use a structured approach to assess coverage, prioritize risks, and compare options. Revisit your plan periodically and document decisions so they stay aligned with changing needs. A clear framework reduces stress and leads to smarter insurance choices.